Payments and the ability to exchange value efficiently and securely over the

web are critical to global commerce. Open standards for payments and value

exchange help ensure open access and interoperability to financial systems for

all the people that use the Web. This document describes aset of capabilities

that, if standardized, will improve payments on the Web.

This document is in early draft state and is expected to rapidly evolve

based on broad feedback and input from the Web Payments Interest Group.

Introduction

This document needs an introduction! - SPM

Relationship to Other Documents

In addition to this document, the Web Payments Interest Group is

developing:

- A

Vision for Web Payments describes the desirable properties of a Web

payments architecture.

-

Web Payments Use Cases 1.0 is a prioritized list of Web payments

scenarios that the Interest Group expects to address via the capabilities

described in this document. The use cases establish a scope of work and a

deeper analysis of implied requirements (technical, regulatory, etc.) will

inform future standardization work.

- A

Roadmap proposes which groups (in or outside of W3C) should take

the lead on creating standards for these capabilities.

Overview of Capabilities

Capabilities are functionalities necessary to implement payments on the

Web. We include capabilities specific to payments but also capabilities that

support payments (such as security) and capabilities more broadly related to

commerce, as it is important to understand the full context in which payments

occur.

We organize capabilities into five groups.

-

Security Core - These capabilities provide the security

foundation for payments.

Capabilities: Key Creation and

Management, Cryptographic Signatures, Encryption

Right now this group has

only security capabilities in it. We may wish to have a more general

purpose Core set. If so, what would this core set include?

-

Trust and Identity - Includes features related to establishing

trust among parties, and credentialing or authorization of parties involved

in a transaction.

Capabilities:

Identity, Credentials, Rights, Authentication, Authorization, Privacy, Discovery,

Registration, Enrollment, and Legal/Regulatory concerns.

-

Accounts and Settlement - Includes capabilities related to

managing stores of value (such as Deposit Accounts) and recorded accounts

of ownership (such as Ledger entries, Deeds, etc.) used as part of the

settlement of payments or commercial exchanges. Settlement via the Web

involves access to the accounts of the participants and ledgers of the

account providers and capabilities to manage accounts and capture and

monitor transactions in a ledger against those accounts.

Capabilities:

Accounts, Ledgers, and Legal/Regulatory

concerns related to accounting and recorded ownership.

-

Payments and Clearing - These are the capabilities that help

parties in a transaction establish the mechanics of how the payment will be

executed and the directly or indirectly make this happen. This involves the

ability to discover and negotiate the mechanism that will be used to

execute the payment and agree on the terms including facts such as the

costs of making the payment, time between clearing of the payment and

settlement into the payee’s account, regulatory requirements and required

authorisations.

Capabilities:

Funding, Payment, Messaging, Clearing, Markets, Foreign/Currency

Exchange, and Legal/regulatory concerns specific to Payments and

Exchange of Value.

-

Commerce - Includes capabilities related to commercial and

economic interactions.

Capabilities:

Offers, Invoicing, Receipts, Loyalty, Rewards,

Contracts, Lending, Insurance, Taxation, Legal/Regulatory concerns related

to aspects of commercial and economic interactions.

The Interest Group anticipates that these groups will make it easier to

define modules that may be reused at a variety of times in a payment

transaction, to prioritize capabilities and craft charters for groups to

standardize them, and to communicate the group’s plans with other standards

bodies and organizations.

Some of these capabilities are expected be useful outside of payment

scenarios.

Digital Wallets and Payment Agents

Although the capabilities described in this document may be used and

composed in a variety of ways to fulfill payments use cases, the Interest Group

anticipates that in many cases, they will be packaged in “payment agents” (or

“digital wallets”) that act as a bridge between the merchant, the user, and the

user’s account providers.

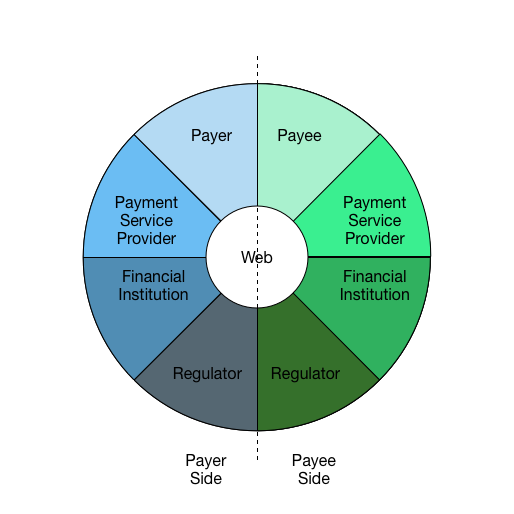

Capabilities in Context

To simplify and harmonize the descriptions of capabilities necessary for

payments and value exchange on the Web, it is helpful to understand the parties

involved and the direction that information flows among them at various

phases of a payment. We use the following diagram to help illustrate

roles and information flow:

Figure: Payment Interaction Wheel

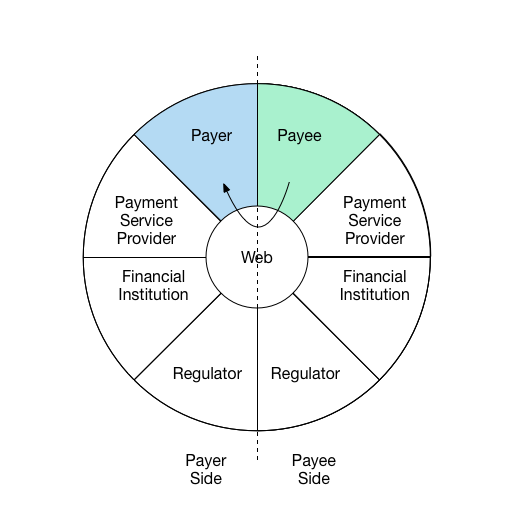

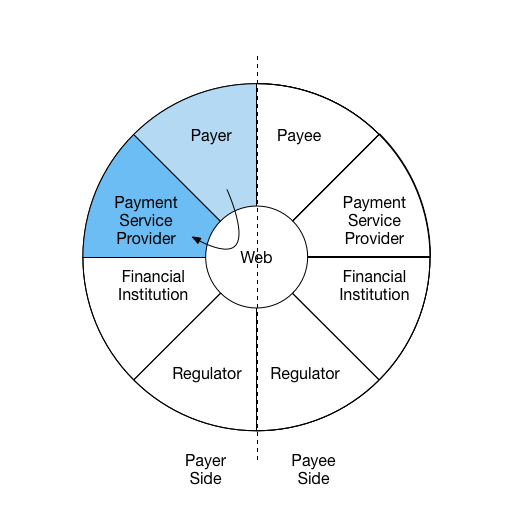

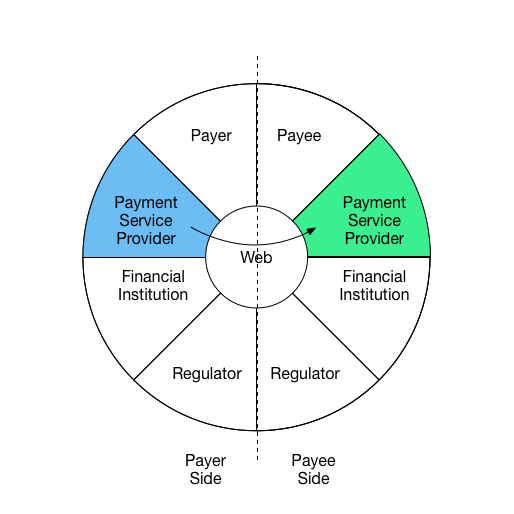

For example, the following diagrams illustrate three interactions in a

comment payment scenario.

Interaction 1:

Payee communicates request for payment to payer and shares payment instructions

Interaction 2:

Payer uses information received from Payee and creates a new payment request

from Payment Services Provider with stored value.

Interaction 3:

Payer’s Payment Services Provider sends details to complete payment to Payee's Payment Services Provider

The roles illustrated here may be carried out by many different entities.

For example, "account provider" may be carried out by financial institutions,

mobile operators, tech companies, or cryptocurrency systems; “payee” may be an

individual, a business, an NGO, or any entity that can accept a payment.

A payment may involve just two parties (e.g., peer-to-peer) or may be

carried out by several collaborating parties. For instance, a payee may use a

payment service provider which in turn uses a card network. The actions of

these intermediaries may vary, from simply forwarding messages to fulfilling

regulatory obligations. Additionally, these interactions may happen in

different sequences and direction depending on the payment context.

Capabilities in Detail

Core and Security

- Key Management

- All participants require an interchangeable mechanism for creation,

management, storage, and exchange of cryptographic keys

- Key management capabilities are required to:

- Securely communicate unique identifiers of payment process

participants

- Digitally sign and authenticate

information exchanged as part of the payments process (e.g., payments,

receipts, invoices, etc.)

- Provide reference key for independent elements of the payments process to

compose/link transactions and related data across asynchronous segments of

the payment process

- Cryptographic Signatures

- Information transferred should be cryptographically signed

to ensure

- Authenticity of the participants and ownership of value/asset being

transferred or exchanged

- Nonrepudiationof participants intent

related to information / communication being exchanged

Key Concepts:

(describe any key concepts/relationship to other capabilities here)

Suggested Deliverables:

- Data model with a concrete syntax for expressing data in the

architecture

- Web-based key public key infrastructure data formats and

protocols

- New normalization mechanisms for data model serialization (if necessary,

for digital signatures)

- Digital signature mechanism for data model

Related Specifications:

- Data models: Graph (RDF), Document/Tree (JSON, XML)

- Syntaxes: XML, JSON, JSON-LD

- Normalization: XML Canonicalization, RDF Dataset Normalization

- Signatures: Linked Data Signatures, Javascript Object Signing and

Encryption, XML Digital Signature

Responsible Working Group(s) or Standards Bodies:

- Linked Data Signatures Working Group (W3C)

- JOSE (IETF)

Identity and Credentials

- Identity

- Entities in the System are able to access Identity information of other

parties it is interacting with if specifically required by law, or if

consented to by owner of the information

- Identity and credentials of an entity are able to be linked/associated

with Accounts and payments to satisfy requirements for Account Providers and

Payments Service Providers to comply with KYC/AML requirements.

- Credentials

- Entities in the system are able to be associated with 1 or more

credentials. A credential is a qualification, achievement, quality, or piece

of information about an entity’s background such as a name, home address,

government ID, professional license, or university degree, typically used to

indicate suitability. Thisallows for the exchange of suitable qualities of

the entity (ex. over age 21) without divulging sensitive attributes/details

about the entity (ex. date of birth)

- Payer is able to exchange standard format credentials with Payee to

validate attributes necessary to complete the payment

- Rights

- Authentication

- Participants are able to authenticate the validity of identifiers

presented by entities that they are interacting with

- Authorization

- Privacy

- All capabilities in this document should be standardized in a way that

minimizes the inclusion/exchange of personal or other sensitive metadata that

are part of the payments process unless specifically required by

law, or consented to by the owner of the

information.

- Discovery

- Payer is able to securely locate public identifier of Payee to be used as

part of payment process

- Payee is able to obtain public identifier of Payer participating in

payment process

- Payer identifier is persistent across devices

- Registration

- Payer and Payee able to register with Payment Services

Provider to obtain

credentials used for payments process

-

Enrollment

- Payment services provider is able to perform the necessary steps during

payer/payee enrollment to collect required identity and credential

information about the payer/payee and associate it with an Account.

- Legal/Regulatory concerns related to Trust and Identity

Key Concepts:

TO DISCUSS: Trust Agent???

Suggested Deliverables:

- Data format and vocabularies for expressing cryptographically verifiable

credentials

- Protocol to issue credentials to a recipient

- Protocol to store credentials at an arbitrary location as decided by a

recipient

- Protocol to request and transmit credentials, given a recipient’s

authorization, to a credential consumer

- Protocol to strongly bind an identifier to a real world identity and a

cryptographic token (ex: two-factor hardware device)

- Protocol to request and deliver untraceable, short-lived, privacy

enhancing credentials.

- Protocol to discover entity’s credential service

Related Specifications:

- Identity Credentials (Credentials WG)

- Credentials Vocabulary (Credentials WG)

Responsible Working Group(s) or Standards Bodies:

- Credentials Working Group (W3C)

- Authentication Working Groups (W3C)

Accounts and Settlement

Accounts

-

Manage Accounts

- Payers and Payees (account owners) require the capability to create

accounts at an account provider.

- Payers and Payees require the capability to authorise access to their

accounts by third parties such as Payment Services Providers.

- Payers, Payees and other authorised entities require the capability of

checking the current balance on an account.

- Account Registration/Enrollmentat Payments Services Providers

- Payers and Payees are able to register accounts that will be used as part

of the payment process with Payment Services Providers of their choice

- Payers and Payees are able to delegate access to specific account

functions to Payment Services Providers of their choice

- Receive Funds

- Payees are able to receive funds into theiraccounts

- Send funds

- Payers are able to transfer funds from their accounts

Key Concepts:

(describe any key concepts/relationship to other capabilities here)

Suggested Deliverables:

(include suggested/needed deliverables here)

Responsible Working Group(s) or Standards Bodies:

Related Specifications:

(Insert relevant related existing or in progress standards for capability

segment)

Ledgers

- Discovery of Ledger services

- Participants require the capability to locate the endpoints at which

ledger services are offered by an account provider

- Participants require the capability to discover which services are

available against a ledger at an account provider

- Capture transactions in ledger

- Participants in the settlement process require the capability to

capture a transaction in a ledger transferring value from one account to

another on the same ledger.

- Monitor a ledger

- Participants in the settlement process require the ability to

monitor a ledger for new transactions that impact a specific

account.

- Reserve funds in an account

- To execute settlement across ledgers a counterparty may require the

ability to request that an account provider temporarily reserve funds in an

account while settlement is finalised on the other ledger(s).

Suggested Deliverables:

- Standardised data model for accounts and ledgers

- Standardised interface for account management

- Standardised interface for ledger services

- Protocol for discovering ledger services

- Protocol for executing settlement between participants on the open

Web

Related Specifications:

- ISO20022 / X9 specs

- Web Commerce Formats and Protocols (Web Payments WG)

- Web Payments Vocabulary (Web Payments WG)

Responsible Working Group(s) or Standards Bodies:

- Web Settlement Working Group (W3C)

Payments and Exchange

- Payment Instrument Discovery and Selection

- Payer and payee are able to discover payment instruments/schemes which

they have in common and may be used in the payment process

- Payer is able to establish the different costs of making the payment

using the various combinations of payer and payee instruments and schemes

(payment methods)

- Payer is able to select payment instrument for use in the payment

process

- Payee is able to communicate requirements(or preference) to payer as to

whether a specific instrument is accepted and the payment terms for using

that instrument

- Payment Initiation

- Payer is able to initiate a payment using selected payment

instrument

- Payer is able to identify Payee via:

- Information received via Invoice

- Individual contact information

- Information from past payees

- Payee is able to initiate a request for payment to payee’s designated

account provider

- Account provider is able to initiate a payment on behalf of the Payee

based on Payee’s requested schedule and frequency (recurring

payment)

- Payment Authorization

- Payment service provider or payee is able to get authorization from payer

to execute payment either in real-time or using a preloaded authorization

mechanism

- Payment service provider is able to demonstrate to payer account provider

that payment is authorised

- Payment Execution

- Payment orchestrator is able to evaluate that all requirements have been

met to execute the payment including authorization(s) and compliance checks

as required.

- Payment orchestrator is able to instruct all participants to execute the

payment and perform any roll-back steps that may be required in case of a

failure by any participant to complete the payment.

- Payment Acknowledgement

- Payee is able to receive confirmation that payment has been successfully

completed

- Payer is able to receive verification that payment has been successfully

received

- Account provider is able to receive confirmation that payment is

complete

- Regulatory/Legal Compliance

- Regulator is able to access/view required payment, payer, and payee

details for payments that take place within their jurisdiction

- Regulator is able to intervene in payments meeting or exceeding certain

thresholds or criteria in order to comply with jurisdictional laws and

requirements

- Payment Settlement and Clearing

- Payment service provider is able to provide payer with

quotesto settle payee via all payee

supported payment schemes

Key Concepts:

TODO: Payment Agent

Suggested Deliverables:

- Protocol for discovering all payment instruments available to a

payer.

- User Agent API and REST API for initiating a payment and protocol for

routing an invoice to a payment service

- Protocol for authorizing payment via regulatory API

- User Agent API and REST API for completing a payment and protocol for

routing payment acknowledgement to payer

Related Specifications:

- ISO20022 / X9 specs

- Web Commerce Formats and Protocols (Web Payments WG)

- Web Commerce User Agent API (Web Payments WG)

- Web Payments Vocabulary (Web Payments WG)

Responsible Working Group(s) or Standards Bodies:

- Web Payments Working Group (W3C)

Commerce

Offers

- Generate Offer

- Payee is able to generate a standard format offer which provides

information on specific products or services being offered, and additional

information on payment instruments accepted, or terms of the offer.

- Payer is able to generate a standard format offer which can be accepted

or declined by the payee.

- Payee is able to create scheduled/recurring offers

- Receive Offer

- Payer is able to receive offer in machine readable format and use it to

initiate payment request

- Payeeis able to receive offer in

machine readable format and use it to create invoice

Discounts

-

Payee is able toable tocommunicate discounts which may be applied to

Offers

-

Payee is able to receive and apply discount to offer

-

Payee is able to apply standard loyalty identifiers to offers

Coupons

- Payer is able to apply coupons to offers

- Payee is able to issue general use coupons

- Payee is able to issue coupons specific to payer identifier

Suggested Deliverables:

- Data format and vocabularies for expressing offers and coupons

- User Agent API for using an offer to initiate a payment

Related Specifications:

- Web Commerce Formats and Protocols (Web Payments WG)

- Web Commerce User Agent API (Web Payments WG)

- Web Payments Vocabulary (Web Payments WG)

Responsible Working Group(s) or Standards Bodies:

- Web Payments Working Group (W3C)

Invoices

- Invoice creation

- Payee is able to generate a standard formatted invoice

and communicate to Payer as part of the negotiation

of payment terms

- Invoice receipt

- Payer is able to receive standard formatted invoice

- Invoice data

- Invoice provides payer with Payment instructions for making payment to

Payee

- Invoice identifier is returned to Payee via payment process to verify

payment is complete

Suggested Deliverables:

- Data format and vocabulary for expressing an invoice

- User Agent API for initiating a payment and protocol for routing an

invoice to a payment service

Related Specifications:

- Web Commerce Formats and Protocols (Web Payments WG)

- Web Commerce User Agent API (Web Payments WG)

- Web Payments Vocabulary (Web Payments WG)

Responsible Working Group(s) or Standards Bodies:

- Web Payments Working Group (W3C)

Receipts

- Create Receipt

- Payee is able to create receipt and communicate receipt to Payer

following completion of payment

- Receive Receipt

- Payer is able to receive receipt and persist for future use

(ex. returns, reimbursement, etc)

Suggested Deliverables:

- Data format and vocabulary for expressing a receipt

- Protocol for routing an receipt to a payer’s receipt storage service

Related Specifications:

- Web Commerce Formats and Protocols (Web Payments WG)

- Web Payments Vocabulary (Web Payments WG)

Responsible Working Group(s) or Standards Bodies:

- Web Payments Working Group (W3C)

Loyalty

- Payer is able to register with Payee’s loyalty program by requesting

loyalty identifier from Payee.

- Payee can “opt-in” to loyalty program by providing program specific

public identifier

Suggested Deliverables:

- Same as “Trust” deliverables

Related Specifications:

-

Identity Credentials (Credentials WG)

- Credentials Vocabulary (Credentials WG)

- Web Commerce Vocabulary (Credentials WG)

Responsible Working Group(s) or Standards Bodies:

- Credentials Working Group (W3C)

Guiding principles and key considerations

Due to the breadth of the capabilities that will require standardization, it

is important to outline certain guiding principles which are expected to be

incorporated across each of the defined capabilities in this document as they

are undertaken by standards teams. The principles include:

Extensibility

- Because the Web payments architecture will accommodate a great variety of

payment schemes (existing and new), we expect to future standards to support

interoperability on a minimal set of features and also support

scheme-specific extensions. Therefore, data formats must be easily

extensible.

Composability

- Different parties will want to add information to messages that are

forwarded.

Identifiers

- Payment schemes define identifier syntax and semantics (e.g., primary

account numbers (PANs) for credit cards, or bitcoin account identifiers). We

expect to support scheme-specific identifiers. But where global identifiers

are required and are not scheme specific, we expect to use URIs.

- Due to the nature of payments and the fundamental challenge of preventing

“double-spending” as part of the payments process, it is important that every

actor/system be uniquely identifiable to other actors and systems

participating in the payments process. While each actor must be identifiable,

a number of use cases that need to be addressed include low value or

less-sensitive payments which do not require the knowledge of a participant’s

identity as a part of the transaction. Because of this, it is important to

de-couple the identification (non-identity based unique ID) of each

participant in the Architecture from the Identity data (sensitive/private

data about the participant) which describes information about a participant

taking part in the system

Security

- Messages must not be altered in transit, but may be included as part of

encapsulating messages created by intermediaries.

- It must be possible to provide read-only access to transaction

information to third parties (with user consent).

- Signatures must be non-forgeable.

Identity, Privacy, and Consumer Protection

- To satisfy regulatory requirements and financial industry expectations,

some use cases will require strong assurances of connections between a Web

identity and a real-world identity.

- At the same time, any source of information that can lead to the

unintended disclosure or leakage of a user’s identity (or purchasing habits)

is likely protected in a jurisdiction somewhere in the world by a

legal/regulatory entity having responsibility for its citizens.

- For discussion: the role of per-transaction pseudo-anonymous identity

mechanisms for some use cases. These mechanisms would make it much more

difficult for an unauthorized party to track a user’s purchasing habits from

1 transaction to another transaction. This will also eliminate the loss of

that identity from affecting other services that user is enrolled in.

- Regulations in several jurisdictions require the consumer to be notified

every time their personal information/credentials are accessed. To discuss:

cryptography requiring a user’s input/knowledge to open that

information.

- Some purchases in combination (e.g., products accommodating prenatal care

needs) will leak sensitive information. To discuss: dynamic key construction

can be applied to each line item in a receipt to help prevent unauthorized

data mining of individuals, legal & regulatory snooping. Even if the

protected information is stolen or accidentally forwarded to unauthorized

parties they will not have the correct tokenized inputs to recreate the

dynamic keys to unlock access to the protected information.

- Role based access controls when applied to dynamic key construction for

each individual credential or large sets of data will help facilitate

interoperable access without needless duplication and encryption of

information for each authorized party. For discussion: Use dynamic keys to

protect a static key where various dynamic keys can be used to unlock the

static key that protects the sensitive content.

- The system should support privacy by requiring only the minimal amount of

information necessary to carry out a transaction. Additional considerations

(e.g., marketing initiatives with user consent, or legal requirements) may

lead to additional information exchange beyond the minimum required.

- Payment account providers must take measures to ensure that account

identifiers are not, on their own, sufficient to identify the account

holder.

- Another suggestion: “Don’t require personal authentication, but make sure

it can be done properly”

Legal and Regulatory

- In some jurisdictions legal or regulatory entities may need to be granted

“time-limited access” to a transaction to view specific credentials and

purchased items of the user. The system should limit what is viewed to the

minimum necessary. Examples: Government subsidies such as food stamps,

controlled substances. In these cases those particular line items in the

receipt may be required to be viewable via individuals or computers charged

with the responsibility to prevent abuse of those programs (e.g.,

unauthorized reselling). There may also be a requirement to view identities

or credentials.

- For certain classes of payments, such as high value or international, it

must be possible to provide role-based access controls to pierce a

pseudo-anonymous identity mechanism so the transaction can be counter signed

by a legal, regulatory, or KYC/AML system yet safeguard against disclosing

unnecessary information. It must be infeasible for the piercing of this

mechanisms to leak enough information for those authorities to forge user

information.

Accessibility

- Web payment schemas, interfaces, data and the architectures that enable

them need to be made accessible for people with disabilities. Web APIs and

applications must be developed and implemented with accessibility-in-mind and

allow for accessibility features. If not, developers, payees, providers and

retailers may be in violation of disability laws.

Discovery and instrument selection

- Default expectation for privacy reasons is that payee will present

accepted schemes and computation of intersection (or other compution) will

happen on the payer side.

- There are other scenarios to discuss that would presumably involve user

consent (e.g., computation done on payee side, or by a third party

platform).

- Manual card entry will be with us for a while. When there is no digital wallet, the working group should discuss (and possibly recommend good practice) for dealing with the case where there is no registered digital wallet. For example, one idea was for browsers to offer a sort of "transient digital wallet" that acts within the protocol to handle manual data entry.

- Quoting Adrian Hope-Bailie idea: “The algorithm MUST not prevent any

scheme from being available as a candidate for registration AND for this

matching/discovery process. i.e. It shouldn't be possible for the browser (or

any other component that executes this discovery process) to exclude schemes

or instruments on the basis of anything but technical incompatibility.”

- The standard should not hard-code a selection process. Regulatory and

cultural preferences may vary (e.g., the

Alibaba escrow use case).